Applying for a Credit Card without Affecting Your Credit Score: A Guide for Expats in the US

Discover how to check credit card eligibility through soft inquiries and pre-approvals—avoiding the 5-10 point score drop that comes with hard pulls.

Updated for 2026: This post was originally published in 2023. For the latest strategies and a comprehensive guide, see Building Credit in the US as an Expat: The Complete 2026 Guide.

When I first started building my credit in the US, I was terrified of doing anything that would hurt the tiny score I had managed to accumulate. After 15+ years in Singapore where credit cards just... worked, landing in America with essentially zero credit history was a humbling experience T.T

I remember wanting to apply for a better rewards card but hesitating because I had read that applications can lower your score. So I spent a lot of time researching how to check eligibility without actually hurting my credit. Here is what I figured out — I hope it saves you some of the anxiety I went through.

Understanding how applying for a credit card affects your score

When you apply for a credit card, the lender performs a credit check to assess your creditworthiness. This can be either a hard inquiry or a soft inquiry, and the distinction matters a lot.

Hard inquiries happen when you formally apply for a loan or credit card. They stay on your credit report for two years and can lower your score by about 5 to 10 points. The drop is temporary and usually recovers in a few months, but when your score is already fragile (as it tends to be for new expats), every point feels precious.

The reasoning is that hard inquiries signal you are actively seeking new credit, which lenders interpret as potential risk. I think this makes sense from their perspective, even if it feels a bit unfair when you are just trying to establish yourself in a new country.

Soft inquiries, on the other hand, do not impact your score at all. These happen when companies check your credit for pre-approval offers, or when you check your own score. This is the route you want to take whenever possible.

Ways to check eligibility without a hard pull

Pre-approval offers

Pre-approval offers are credit card applications where the lender has already done a soft inquiry to determine if you are likely eligible. You might get these in the mail or email. The important thing to understand: the pre-screening itself is a soft pull. But if you decide to actually apply, a hard inquiry will be performed.

To get pre-approval offers:

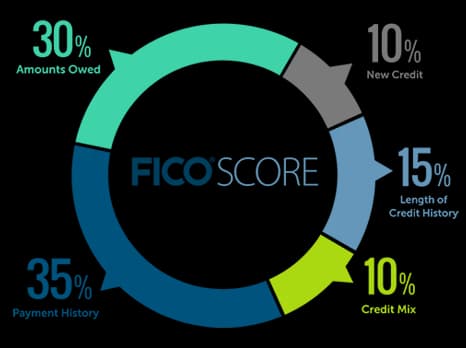

- Check your credit score first. Use your banking apps or sign up for free accounts with the three main credit bureaus (Equifax, Experian, and Transunion). (Need a refresher? I wrote about understanding your FICO score as an expat.)

- Sign up for credit monitoring services. Credit Karma is great for this — it alerts you when new pre-approval offers become available, sometimes tailored to your specific score.

- Check directly with card issuers. You can use Chase's pre-approval form or Capital One's pre-approval tool to see if you qualify before committing to a hard pull.

Store credit cards

Store credit cards are generally easier to get approved for. They are often offered during checkout, and some do not require a credit check at all. They can also offer exclusive discounts.

However — and this is worth knowing — store cards typically have lower credit limits and higher interest rates. They can only be used at that specific store, and the sign-up bonuses are usually not as attractive as regular rewards cards. (For a deeper look at rewards cards, check out this post.)

Secured credit cards

This is where most newly arrived expats will likely start, and that is completely normal. Secured credit cards are designed for people with limited credit history. You put down a security deposit that becomes your credit limit. The application typically involves only a soft inquiry.

I wrote a detailed article on how to build credit as an expat. With some discipline and a bit of luck, your score can jump to 720+ within about five months. (I cannot guarantee anything, of course — do your own research to make informed decisions.) For a deep dive into secured credit cards specifically, I have that covered too.

Checking for soft inquiry offers

Before applying for any card, check whether the lender offers a soft inquiry option. This is more common when you already have an existing relationship with the card issuer. From my experience, having a checking or savings account with a bank made a real difference in what they were willing to offer me without a hard pull.

Are soft-pull credit cards worth it?

I have to be honest here — generally, the best rewards cards (travel cards, premium cash-back cards) require a hard pull. And since the impact of a hard inquiry is temporary, soft-pull credit cards are often not worth pursuing unless you have no other choice. I think of them more as a stepping stone than a destination :)

Quick FAQs

How much does your credit score drop when you apply?

From my research, a single hard inquiry typically drops your score by about five points or less. The impact is temporary.

Is pre-approval bad for credit?

No. Pre-approval checks are soft inquiries and do not affect your score.

Does signing up for Credit Karma hurt your score?

No. Checking your scores through Credit Karma, the credit bureaus directly, or your banking apps does not impact your score at all.

Is a pre-approved offer guaranteed?

Unfortunately, no. Pre-approved means your chances are high but not 100%. From my experience, pre-approval from a bank where you already have an account carries a much higher success rate, since they already know you as a customer.

Pre-approval is also stronger than pre-qualified. Pre-qualified basically means the issuer has made an educated guess that you might be approved.

Is there a credit card that approves everyone?

I do not think so. Secured credit cards from your current bank are typically the easiest to get — start there.

How many soft inquiries are too many?

Since soft inquiries do not impact your score, there is no limit to worry about. Check away :D

Wrapping up

Applying for a credit card without damaging your score is definitely possible — it just takes a bit more patience and research. Focus on pre-approvals and soft inquiries first, and do not stress too much about hard pulls when you are ready for a better card. The temporary score dip is worth it for the right rewards card.

The credit system in the US felt like a maze when I first arrived. But I promise, it gets easier once you understand the rules of the game.

What has been your experience navigating credit cards as an expat? Any surprises I did not cover?

Cheers,

Chandler

P.S. I recently created a group on Facebook called Asian Expats in the US so that we can share and discuss more tips directly. Feel free to join.